I sold all our shares of GEE Group this quarter. In my last letter, I mentioned how GEE Group’s place in our portfolio was dependent on management’s commitment to using the company’s balance sheet cash for the benefit of shareholders. Well, another quarter came and went with zero evidence that management’s promises and assurances were anything but empty words.

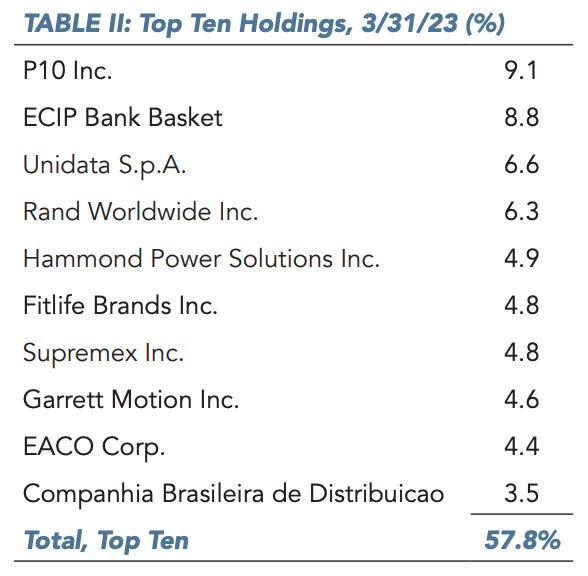

Hammond Power

In happier news, I have identified another opportunity in the Canadian industrial sector. Small Canadian manufacturers have become something of a theme for Alluvial, first with Supremex and now with our new holding Hammond Power Solutions. For decades, Hammond Power Solutions has been producing transformers, the boring, but utterly essential components responsible for transferring energy between circuits in electrical installations.

Despite the stellar outlook, Hammond Power shares change hands at below 10x trailing earnings and the enterprise is valued at 7x operating income. 2023 earnings will increase from last year’s as a result of price increases and continued strong demand. Hammond employs a conservative capital structure with zero debt and produces free cash flow like clockwork.

ECIP Bank Basket

We are invested in a handful of banks, all recipients of low-cost permanent capital courtesy of the US Treasury’s Emergency Capital Investment Program. While the goal of this program was to encourage lending in economically disadvantaged areas, it also happened to make its recipients some of the nation’s best-capitalized banks in terms of total equity to assets. For that reason, there is no cause for concern regarding the safety of any of the banks that Alluvial Fund holds. The market seems to agree as the share prices of our four banks fell just 1% on average this quarter.

Each of our banks trades at a mid-single digit multiple of this year’s earnings and at a discount to economic book value, which I calculate by discounting the value of the ECIP capital infusion at market rates. I continue to believe that each bank will be valued at 2-3x current prices in a few years’ time.

P10

Our largest position remains P10 Inc., which reported another quarter of growth in assets under management, bringing the total to $21.2 billion, up 23% year-over-year. P10 shares are down year-to-date, no doubt reflecting investor pessimism around the fundraising environment for alternative asset managers. And yet, P10 just announced that its subsidiary RCP Advisors succeeded in raising $328 million for RCP XVII, exceeding the targeted $300 million.

Despite the headwinds, P10’s managers are still attracting new capital. Though P10 has not found any suitable acquisitions of late, the company has found value in its own shares, repurchasing 1.6% of shares outstanding in the fourth quarter alone. The logic of these buybacks is unassailable; try as I might, I cannot find a better opportunity on a reward-per-unit-of-risk basis than P10 shares at under 12x perfectly visible, contractually guaranteed recurring free cash flow.

Unidata SpA

Unidata SpA remains a large holding and distinctly under-valued. Shares were pressured earlier this year by the company’s equity offering in support of its acquisition of TWT Group. Adding TWT will be tremendously accretive to Unidata’s earnings and cash flows, but the market is taking a “wait and see” approach. Unidata also announced it had signed a contract for the construction of its new undersea cable, which will be operational in two years’ time. Finally, Unidata has applied to uplist to the Borsa Italiana’s STAR segment, a more prominent segment with higher listing standards that should bring additional attention to the company and its shares.

EACO Corp

I must take a second to recognize EACO Corp., which has quietly become a significant holding for Alluvial Fund. I last mentioned the company almost three years ago when shares were trading around $19. The company was valued around $100 million and had produced operating income of $12.3 million in the trailing year. Today, EACO shares change hands in the low $30s. The company is valued at $140 million and produced operating income of $28 million for the year ended February 28, 2023. Impressive, and still extremely cheap.

Polish Stock Basket

TIM SA, a member of our basket of Polish stocks, received a takeover offer in late March, causing shares to jump 28%. I sold our holdings in the following days. Our investment in TIM was successful but alas, too brief. I had hoped to hold our shares for quite some time and to sell them years down the road at a significantly higher price. However, I cannot blame management for wishing to engineer a fair outcome for shareholders when the market stubbornly refused to recognize TIM’s progress. I am working to invest the proceeds of our TIM SA investment into other Polish securities, which offer some of the world’s best valuations. Other stocks in the Polish basket include Hortico SA, a growing gardening supplier trading at <4x earnings; Auto Partner SA, a high-quality auto parts distributor growing at 30% but trading at 12x earnings; and a new holding in a software company that grew 90% in 2022 but trades at <8x normalized cash flow.