The Rational Cloning: Weekly Ideas #79

Old West on ValueInvestor Insight [Copper, Tin, Bunge, WildBrain]; Some Tweets That Make You Go… Hmm 🤔

Welcome to the 79th edition of the Rational Cloning Newsletter (Weekly Ideas Series).

Helping you discover the best ideas of others.

Happy cloning.

Weekly Investment Ideas

(1) ValueInvestor Insight: Old West Investment Management

You’ve been active in mining stocks where you see clean-energy-driven demand and constrained supply working to companies’ advantage. To get a sense of how you might play that, describe your interest in a company like Filo Mining [Toronto: FIL].

Brian Laks: Copper is a metal we believe will be in significant demand driven by electrification and other clean-energy initiatives, while supply will be challenged by underinvestment in exploration and by declines in average copper grades making mines less productive. In such an environment a large high-grade discovery of copper is a big deal, and that’s what caught our attention with Filo Mining.

The company in 2021 announced what could be a generational discovery of copper resource at its Filo del Sol deposit in Argentina. What made that more interest ing to us is the involvement of the Lundin Group, which owns one-third of the company. Adolf Lundin was a Swedish entrepreneur who built an oil and mining empire in the 1970s that has grown under the leadership of his sons and grandsons. This is not an early-stage project run by promoters – we think they have the experience and the deep pockets to bring this project to production into what will be a highly favorable pricing environment.

We couldn't think about investing in a company at this stage of its development without confidence that the many operating and financing decisions to be made for Filo to ultimately succeed were being made by owner managers with the expertise to pull it off. Their geologists now believe they're developing essentially a new mining district that will support multiple projects. In one very positive sign, BHP early last year invested C$100 million for 5% of the project – paying a premium to the prevailing share price – and agreed to form an advisory committee to help guide its development.

The company’s shares at a recent price of C$23 have more than doubled since they started trading in October 2021. How do you think about valuing a stock like this?

BL: The company in 2019 delineated a development project with a pre-feasibility study on the reserves defined at that point. That was before further exploration indicated the resource base was far larger. At current copper prices and assuming only the reserves they originally defined, we estimate the net asset value here at about C$2.5 billion, which is roughly the current enterprise value. It’s typical for the market not to give full credit to non-producing reserves, but given the magnitude of the additional discoveries, we think the discount here today is way too large.

Explain your bullish case for tin producer Alphamin Resources [Toronto: AFM].

BL: We typically focus on niche commodities where supply/demand imbalances can form with relative ease, leading to current or expected shortages. It could be that supply is falling due to natural depletion or there's a lack of development investment when prices are low Also, technology developments may lead to increased demand for certain materials faster than supply can respond. This has been the case for a variety of specialty metals necessary to enable the global transition to clean energy, and one of which that isn’t talked about as much is tin.

The global tin market is small, only 2% the size of copper, but it’s essential to manufacturing electronic devices. The largest use is in solder, the conductive material that connects electronic components in printed circuit boards. So demand for tin is strongly tied to semiconductor demand, which has a number of long-term growth tailwinds from the build out of things like advanced telecom networks, datacenters, interconnected devices and electric vehicles. Another example of a new demand driver is solar ribbon, which is copper wire that has been coated in tin and is used to connect individual solar cells on solar panels.

At the same time, the supply situation is fragile. China and Indonesia control roughly half of the market and have seen their production decline over the last two decades. In China much of the production is in the southwestern province of Yunnan, where extreme weather and rising energy prices can lead to power rationing that impacts tin supply. Indonesia has mined much of its onshore resources and miners have been forced into shallow offshore waters to dredge alluvial tin. The thirdlargest producer, Myanmar, is politically unstable and has also seen much of its high-grade discovery depleted. In general, even when tin prices last year hit highs of $50,000 per metric ton, there were not many high-quality development projects in the works to fill the growing supply gap.

The price of tin is still extremely volatile. From $50,000 per ton last year, the price hit $20,000 earlier this year and is now around $25,000. But we see shortterm volatility within the context of a longer-term secular growth in demand combined with a growing supply/demand imbalance. In our view, today’s price is unsustainably low. Not enough production is profitable to meet current levels of demand, let alone where demand is expected to grow. That gets us excited about a company like Alphamin long-term.

How are you looking at valuation from today’s C$0.90 share price?

BL: Even though the price of tin today at $25,000 per ton is at a level where much of the industry is unprofitable, because Alphamin’s all-in production costs are under $15,000 per ton it is still nicely profitable. Using rough numbers, at 20,000 tons in annual production when they turn on the second mine later this year, the company can earn close to US$200 million in EBITDA. That on today’s US$650 million enterprise value gives you an EV/EBITDA multiple of less than 3.3x.

And that’s at today tin price, which we think is unsustainably low. At the $50,000 price level just from last year, the company would be earning more in EBITDA per year than its current enterprise value. From today’s share price, we don’t need heroic multiple or tin-price assumptions to see very significant upside in the stock.

Some Tweets That Make You Go… Hmm 🤔

https://twitter.com/Mr_Neutral_Man/status/1644354042162757633?s=20

https://twitter.com/chriswmayer/status/1644333958203670532?s=20

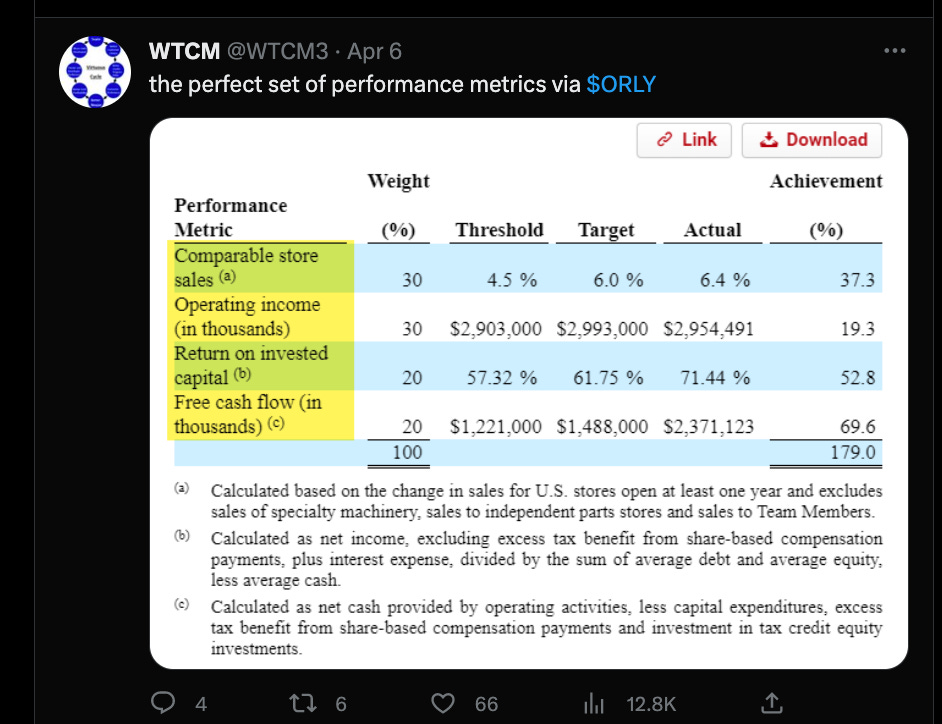

https://twitter.com/WTCM3/status/1644004744162160640?s=20

https://twitter.com/NeckarValue/status/1643659161652035602?s=20

https://twitter.com/AltaFoxCapital/status/1643776964098924544?s=20

Check out previous issues of Weekly Ideas👇

The Rational Cloner’s Library

Mosaic Musings #2: Disinflation → Inflation Inflection Point?

Mosaic Musings #3: Royalty Companies: Inflation, I win; Disinflation, I Don’t Lose Much.

published accidentally incomplete?

no ideas?