The past year made clear that the Fed’s priority was nurturing the asset bubble more than preventing inflation from accelerating. What if everything the Fed has done to preserve the economic illusion comes crashing down along with their credibility? Such bearish outcomes have been predicted for years, and since they haven’t come true, the Fed has been increasingly emboldened.

While there are many things for stock investors to be concerned about today—inflation, rising interest rates, debt, tough earnings comparisons, and war—valuations appear to imply that none of these will derail the bull market. We worry that the perspective of too many investors has been biased by their recent experience when buying dips is always rewarded. Turn on the TV, read financial websites, or talk to friends, and the message is the same: buy stocks and you’ll float too! Far be it from us to stand in front of those chasing returns, but we sincerely hope they aren’t blind to the attendant risks. We’re all living with a bubble.

How many are living in the bubble?

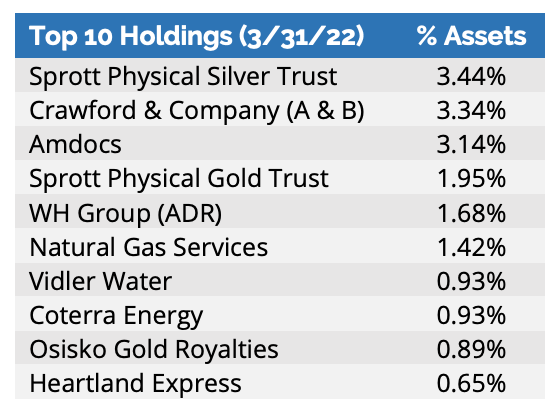

The Fund benefited from the flight to hard assets in Q1. Our energy, gold, and silver securities appreciated during the beginning of the quarter while most other stocks were falling, and we reduced our positions. We sold completely out of Dril-Quip (ticker: DRQ) and Triple Flag Precious Metals (ticker: TFPM.U) after they reached our valuations, although neither was a large holding. Commodities sold off into quarter end, when we had a smaller, but still important, weighting. There were no positions negatively impacting the Fund by more than 10 basis points during the quarter. The top three contributors to the Fund’s first quarter return were Coterra Energy (ticker: CTRA), Sprott Physical Silver Trust (ticker: PSLV), and Amdocs (ticker: DOX).

We acquired three new stocks over the first quarter: Heartland Express (ticker: HTLD), Preformed Line Products (ticker: PLPC), and Miller Industries (ticker: MLR). While many of the companies on our buy list fell in Q1, they were generally declining from lofty levels. The prices did not reach a level where we believed we could meet our required return threshold. Additionally, stocks partially rebounded in the last two weeks of March.

Founded in 1978, Heartland Express (HTLD) is an established short-to-medium haul trucking company serving the entire United States. Since going public in 1986, Heartland has grown revenues from $22 million to $607 million in 2021. Heartland has differentiated itself by keeping its equipment new and deliveries on time. As an efficient provider of premium transportation services, Heartland has a long history of generating above average profit margins and has received multiple customer service awards.

Preformed Line Products (PLP) makes products that protect, connect, terminate, and secure cables and wires for energy, communications, and cable networks. The products are often used to revitalize aging infrastructure to reduce lost revenue from events like malfunctioning power lines or fiber optic cables. Approximately 70% of U.S. transmission lines are over 25 years old, and many are well past their original life expectancy. Repair work occurs after emergencies or natural disasters such as hurricanes, tornadoes, and floods. The 75-year-old company has established a strong competitive position by investing in technology and manufacturing its own products.

Miller Industries (MLR) is the world’s largest manufacturer of tow trucks and is based near Chattanooga, Tennessee. Its only major domestic competitor is Jerr-Dan, a division of Oshkosh Corporation. Miller has grown towing equipment revenues at a 10% organic compound annual rate since exiting its towing services operation in 2003. The company invested heavily in modernizing and expanding its U.S. manufacturing facilities, and the firm also sells to European customers. Demand for tow trucks is primarily connected to miles driven of U.S. vehicles and the age of the fleet. Miller’s earnings fell significantly but remained positive during the 2008 recession, when tow truck operators who buy from the company’s distributors found it more difficult to finance purchases. Miller’s stock initially held up well during the COVID pandemic, despite temporary business pressures. The shares peaked at $47 in April 2021 but retreated below $30 in 2022. Tangible book value per share is $24.

Incredible content. It’s like the Rational Cloning has somehow figured out the best ideas for my brain before I know it. 🙏