There are several reasons we think our portfolio still has meaningful upside, even after a good year

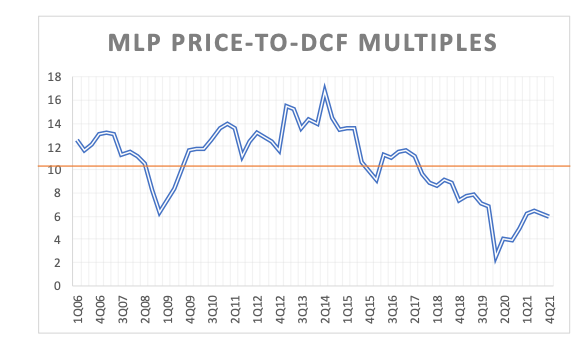

Midstream energy remains cheap. Updating the Distributable Cash Flow chart for 2021 results shows that valuations are still a long way off from historical averages. And while the average can move down if there’s a structural shift in multiples, we’re fine betting there’s still a strong bias against energy that at least partially reverts in time. Over the past 15-years the average DCF multiple is 10.5x and we ended 2021 at 5.9x, suggesting 78% upside to get back to the average. And that math assumes no fundamental improvement in the denominator (cash flows), which is not at all consistent with commodity prices, current E&P activity levels and implied future energy production.

Additionally, although the cumulative return of our portfolio over the past 4-years is positive, the returns in the sectors we’ve been focusing on are not. The Alerian Midstream Index (AMZ) and S&P 500 Energy sub-sector are each down 7% cumulatively, while the NYSE Arca Airline Index (XAL) is down close to 30%. These sectors remain massive underperformers over a multi-year period, so we are still fishing in fertile waters.

If valuations don’t revert closer to the mean, we’ll still get acceptable returns. Remember that DCF is essentially a FCF metric for midstream, but it uses maintenance capex as opposed to total capex. Most of midstream is in maintenance mode and will be for several years as asset utilization increases on existing infrastructure. The cash flow yield on these companies is close to 17% and we own a few with yields over 20%. Whether the cash gets returned through distributions, stock repurchases, or even debt reduction, we don’t particularly care. And while Vistra (VST) isn’t a midstream company it does offer the same value proposition. Shares trade at a 20%+ FCF yield, management pays a modest dividend, gradually reduces debt, and most importantly, is repurchasing over 20% of the outstanding shares over the next year.

We receive a decent amount of cash every quarter from dividends, which allows us to find new opportunities or add to existing positions without having to sell anything. Owning a handful of volatile stocks makes this compelling since several of our positions had a 60%+ dispersion between the 52-week high and 52-week low in calendar year 2021. We think of ourselves as long-term investors, but we have no problem taking advantage of volatility on either side.

The portfolio we own today is hardly the portfolio that got us here. Not one of today’s top 3 positions gained as much as the overall portfolio in 2021. We aren’t counting on outperformers continuing to outperform.

Our portfolio should fare well during periods of high inflation.

Current Portfolio Characteristics

We have fully exited the preferred securities we purchased in March of 2020. Prices converged back to or above par, and while the yields are still decent the upside is limited. This was a highly opportunistic investment and much shorter than we anticipated. We took advantage of forced selling by over levered closed-end funds, which allowed us to buy Crestwood preferred securities yielding 40% and DCP preferreds yielding 59%. We hope we get more opportunities like that in the future.

Another noteworthy change in the portfolio was our shift from solely owning Vistra LEAPs (long dated call options), to building a sizable position in the common equity on the back of the Texas deep-freeze last February. As shares fell into the mid-teens we quickly made it a top position believing that events were an anomaly and could in fact make VST a stronger company in the long-term.

As of year-end the portfolio was heavily weighted to 3 stocks, Enterprise Products Partners, MPLX and Vistra. We like the management team and capital allocation strategy of each company and plan on owning them for a long time. These three provide the ballast of the portfolio while a few smaller investments provide the jet fuel. There are 9 positions in the portfolio, but 2 are not meaningful. The dividend yield is ~6%. Cash is near an all-time low at ~4% but it grows 1.5% every quarter!

Full warning, similar to Armstrong Flooring (AFI), this could be a terrible idea, it has significant red flags and is highly speculative.

LMP Automotive (LMPX) is a micro-cap (~$45MM market cap) that came public in late 2019 with a car subscription model where users could rent a car month-to-month, positioning itself as splitting the difference between a short-term car rental and a traditional car lease. LMPX then put an online dealer/mobile app business model spin around it to market the stock. In 2020, LMPX became a bit of a meme stock, briefly trading up alongside other e-commerce car dealers like Carvana, but then crashed as they were unable to source cars economically to run their subscription model. Instead, the company pivoted to be a traditional car dealership rollup business and went on a debt fueled acquisition spree in 2021. LMPX finished the year with 15 new car dealerships and 4 used car dealerships across 4 states. On 2/16/22, the company said they were unable to secure new financing for their previously announced but not yet closed acquisitions (7 of them!) and quickly pivoted to pursuing a sale:

Sam Tawfik, LMP’s Chief Executive Officer, stated, “The Company intends to terminate all of its pending acquisitions in accordance with the terms of their respective acquisition agreements, primarily due to the inability to secure financial commitments and close within the timeframes set forth in such agreements.”

“The Board of Directors believes that LMP’s current stock price does not reflect the Company’s fair value. Given the record M&A activity in our sector and multiples being paid for these transactions, LMP’s Board of Directors has directed management to immediately pursue strategic alternatives, including a potential sale of the Company.”

The stock closed at $5.25/share on 2/16, it now trades for ~$4.25/share.

Shameless self-plug here (will only be a one-time thing, I promise).

I’ve recently been going through my old notes and polishing them up. Earlier this week, I released my notes on Nick Sleep and Qais Zakaria (Nomad Partnership Letters) on Amazon: